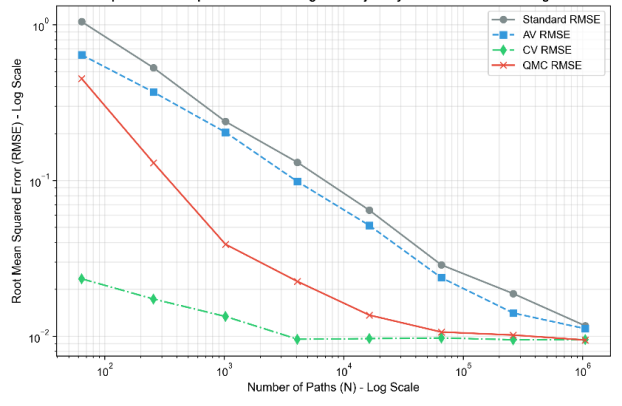

Importance Sampling (IS) is a fundamental variance reduction technique in Monte Carlo simulation, particularly for estimating rare event probabilities. Its core idea is to find a better sampling measureℚunder which the target events occur more frequently, to reduce the cost of simulation of rare events. However, determining such an optimalℚis notoriously difficult, often leading to complicated partial differential equations (PDE) that many classical methods fail. This paper aims to introduce a novel geometric perspective of this optimization problem that we consider all proper likelihood ratios as a manifold, and use the natural gradient property to design the algorithm, which avoids PDE and outperforms the ordinary stochastic gradient descent (SGD) algorithm. Under standard regularity and Novikov conditions, we establish the almost sure convergence of the proposed algorithm utilizing the Robbins-Siegmund theorem and end up with numerical validation on option pricing and portfolio risk assessment, confirming that the geometric approach significantly enhances variance reduction efficiency.

Research Article

Open Access