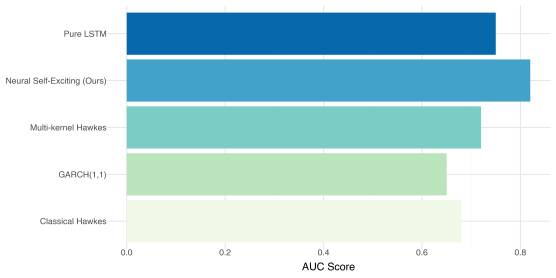

This paper presents a hybrid neural self-exciting point-process model tailored to capture the dynamics of extreme financial shocks. The research background stems from the limitations of classical parametric models in handling nonstationary baselines and the lack of interpretability in purely neural approaches. The primary research objective is to develop a model that couples a learned, time-varying baseline intensity produced by a recurrent encoder with a parsimonious, parameterized self-excitation kernel. The study utilized daily data from three distinct market classes—developed equity (S&P 500), emerging markets (Hang Seng Index), and cryptocurrency (BTC-USD)—over the period 2015–2023. Methodologically, a recurrent neural network captures exogenous drivers, while a parametric kernel models endogenous clustering. Results indicate that this hybrid architecture achieves superior early-warning performance compared to classical Hawkes and GARCH , baselines, particularly in markets with frequent regime shifts. Furthermore, the model provides stable, interpretable memory estimates, such as half-life summaries, which are critical for risk monitoring. The conclusion suggests that hybrid models offer a pragmatic balance between flexibility and interpretability for financial risk analysis.